Do you want to do business in Spain? There are many opportunities in Spain for foreign companies and several ways to start your activity in our country. You have probably heard of two ways, which are the most common, of setting up in Spain: as a branch or as a subsidiary (limited or public limited company). In this post we are going to talk about another alternative, which is the representative office.

What is a representative office?

Index of contents

The representative office is an entity with the following characteristics:

- It does not have its own legal personality independent of the foreign parent company.

- It does not have any administrative bodies either, but carries out its actions through a duly authorised representative.

- The representative office cannot carry out an economic activity (this is its main difference with a branch) and its tasks are usually focused on coordination and collaboration. In addition, it will carry out: market research, preparation of contracts and other ancillary activities.

- The foreign parent company is responsible for the debts incurred by the representative office in Spain.

- It does not have its own capital independent of the parent company, but the parent company may assign it a fund.

How is a representative office constituted?

The opening of a representative office in Spain requires the execution of a public deed (or other document executed before a foreign Notary Public, which is legalised with the Hague Apostille or other system).

The deed will be used for tax, labour and social security formalities and its content is as follows:

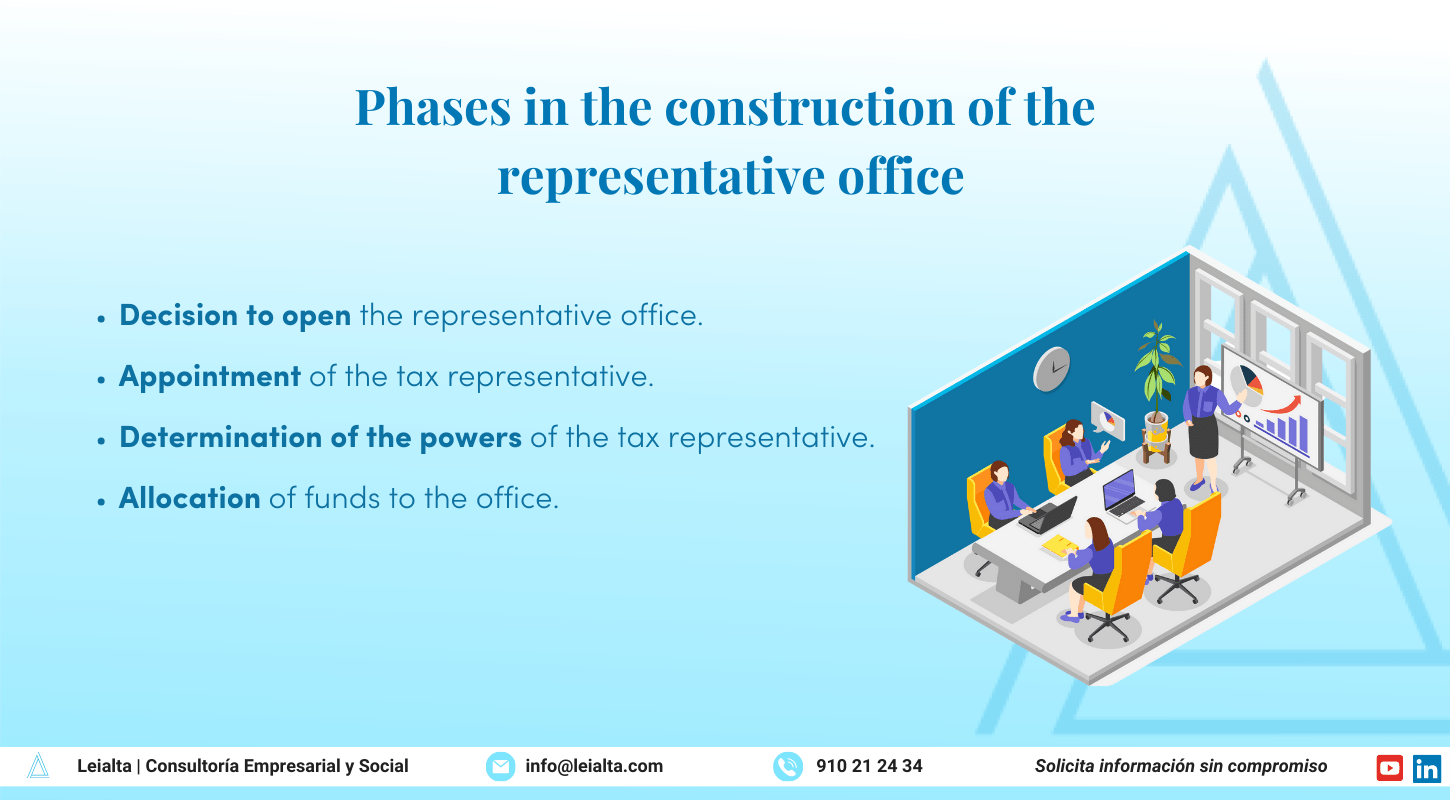

- Decision to open the representative office.

- Appointment of the tax representative (who must be a natural or legal person resident in Spain).

- Determination of the powers of the tax representative.

- Allocation of funds to the office.

It is not necessary to register the representative office in the Commercial Register.

How is the Tax Agency notified of the appointment of the tax representative?

In order to notify the Tax Agency of the appointment of the tax representative, form 036 signed by said representative must be submitted, to which the following documentation must be attached:

- Deed of appointment of the tax representative, formalised before a foreign Notary Public.

- DNI or NIE of the tax representative.

- Document accrediting the existence of the foreign company, which may be:

- A memorandum of association or articles of association of the entity, registered in the commercial register of the country of origin.

- A certificate from a foreign notary or a foreign tax office.

Then, the Tax Agency will assign a NIF and you will be able to operate in Spain.

At LEIALTA we offer a legal and tax representative service for your business, made up of experts from various disciplines (commercial and tax lawyers) who will advise you in several languages. Our service includes the following actions:

- Advice from the start of the activity in Spain.

- Interlocution with the Spanish Tax Agency.

- Carrying out administrative procedures.

- Analysis of compliance with tax regulations.

Is a representative office a permanent establishment?

For Value Added Tax (VAT) and Corporate Income Tax (CIT) purposes, the representative office is not a permanent establishment, but it is necessary to be careful because as soon as the employees carry out commercial work with the capacity to contract with clients, it could be considered a permanent establishment and, therefore, be taxed for VAT and CIT. In this case, the situation and the applicable international conventions should be studied in depth to avoid double taxation.

The accounts of the representative office are kept by the foreign company.

What other ways of doing business in Spain are there?

As we said at the beginning, there are several ways of doing business in Spain, in addition to the representative office:

- Selling directly from a foreign country without having a structure in Spain.

- Hiring an agent in Spain.

- Create a subsidiary. In this case, a trading company is created in Spain that has an independent legal personality with respect to the foreign parent company. The subsidiary must be taxed in Spain for IS and VAT.

- Setting up a branch. It does not have its own legal personality and must keep its own accounts. For example, if you want to rent premises in Spain, the parent company will have to sign and pay the rent. In this case, the branch will also have to pay IS and VAT in Spain.

As you have seen, there are many ways to do business in Spain. The one you choose will depend on the objective you wish to achieve in our country. You can start with a representative office to study the market and analyse the feasibility of setting up your business in Spain, and then open a branch or subsidiary.

Good Article